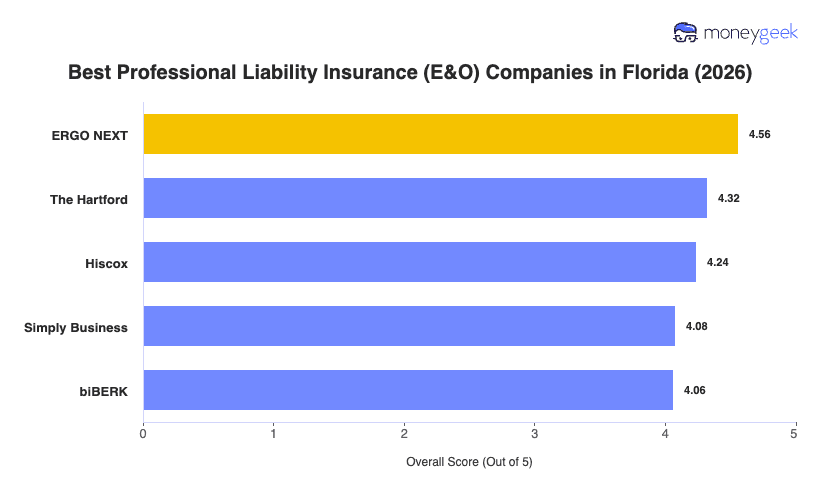

Our analysis of Florida professional liability insurers found three providers that consistently outperformed the field on rates, coverage quality and customer experience.

- ERGO NEXT: A fully digital buying process, 24/7 certificate of insurance access and rates that beat the Florida average by 25% earned ERGO NEXT the top position. The insurer ranks first for professional liability across most Florida industries, including consulting, financial services, healthcare, tech, construction and pet care. Education businesses should look elsewhere, where ERGO NEXT ranks seventh in the state.

- The Hartford: Responsive claims handling and an industry-specific underwriting approach set The Hartford apart, particularly for Florida's beauty, wellness, cleaning, real estate and tech businesses, where it ranks first or second. With more than 200 years in operation, the insurer brings dedicated service teams and a complaint rate 22% below the national average. It underperforms for healthcare and other professional services, where it ranks ninth in Florida.

- Hiscox: Founded in 1901, Hiscox built its reputation on specialist professional liability coverage, and that depth shows for Florida education providers, consultants, nonprofits, financial services firms and childcare operators, where it ranks first or second. Its professional liability policies cover work performed anywhere in the world, which suits Florida businesses with clients across state lines or internationally.

These three providers represent the strongest fit for most Florida businesses, but no ranking captures every variable your situation involves. Comparing business insurance options side-by-side and getting quotes directly from carriers gives you the clearest picture of what your business will actually pay.