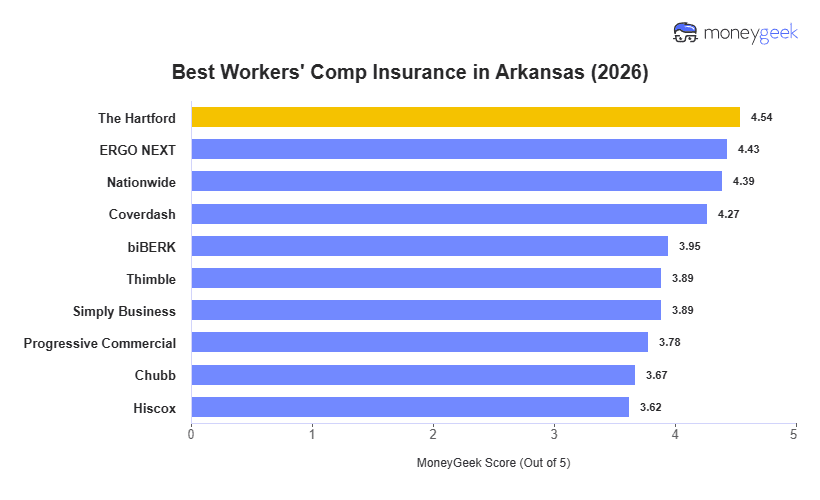

The Hartford tops MoneyGeek's ranking of the best workers' comp insurance in Arkansas, tying with Nationwide for the lowest monthly rate at $49. The Hartford's edge comes from its coverage rank (third) and customer service rank (third), giving it the most balanced profile in the state. ERGO NEXT ranks second overall, with competitive rates and strong customer service, but it ranks sixth on coverage, which matters if your business operates in a higher-risk industry where policy breadth is a high priority.

Best Workers' Comp Insurance in Arkansas (2026)

With monthly rates as low as $8 monthly, The Hartford, ERGO NEXT and Nationwide offer the cheapest and best workers' comp insurance in Arkansas.

Get matched to top Arkansas workers' comp insurance providers and find your ideal coverage.

Select state

Updated: July 20, 2026

Advertising & Editorial Disclosure

Best Arkansas Workers' Comp Insurance: Fast Answers

The Hartford leads Arkansas with the top MoneyGeek score and the lowest monthly rate at $49, making it both the best and cheapest option in the state. Nationwide ties The Hartford for the lowest rate among all ranked providers.

- The Hartford: $49 a month

- Nationwide: $49 a month

- ERGO NEXT: $50 a month

- Coverdash: $61 a month

- Thimble: $62 a month

Arkansas requires workers' comp for employers with three or more employees, a lower threshold than many other states. The Arkansas Workers' Compensation Commission oversees compliance and enforcement across the state. Employers who fail to carry required coverage face stop-work orders and personal liability for the full cost of any employee injuries.

Averaging $65 per month, Arkansas is one of the more affordable workers' comp markets in the region. The cheapest industries are Financial Services and Beauty/Body & Wellness, both averaging $13 a month, while Transportation & Logistics ($192 a month) and Construction ($178 a month) are the most expensive in the state.

Arkansas operates a fully competitive private market, meaning employers can get workers' comp insurance directly from licensed carriers. Employers unable to secure voluntary market coverage can access the Arkansas Workers' Compensation Assigned Risk Plan, administered through NCCI. Qualifying large employers may also apply for self-insurance status under the Arkansas Workers' Compensation Commission.

Arkansas workers' comp policies cover four primary benefit categories:

- Medical expenses: Covers all reasonable and necessary medical treatment for work-related injuries; the Arkansas Workers' Compensation Commission sets the medical fee schedule.

- Wage loss benefits: Pays temporary total disability at 66⅔% of the employee's average weekly wage, subject to the current maximum weekly benefit established by the Arkansas Workers' Compensation Commission.

- Vocational rehabilitation: Covers retraining and placement support for workers unable to return to their pre-injury position.

- Death benefits: Pays burial expenses and compensation to qualifying dependents based on a percentage of the deceased's average weekly wage.

Best Workers' Comp Insurance Companies in Arkansas

| The Hartford | 4.54 | $49 | 3 | 3 |

| ERGO NEXT | 4.43 | $50 | 1 | 6 |

| Nationwide | 4.39 | $49 | 6 | 5 |

| Coverdash | 4.27 | $61 | 5 | 1 |

| biBERK | 3.95 | $65 | 8 | 8 |

| Thimble | 3.89 | $62 | 8 | 9 |

| Simply Business | 3.89 | $73 | 2 | 2 |

| Progressive Commercial | 3.78 | $70 | 8 | 7 |

| Chubb | 3.67 | $91 | 3 | 4 |

| Hiscox | 3.62 | $77 | 6 | 10 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with one to four employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

These overall rankings don't account for industry-specific risk or business size. For trade-specific recommendations, see the guides below.

The Hartford

Best Workers' Comp Insurance in Arkansas

MoneyGeek Rating

4.5/ 5

4.8/5Affordability Score

4.1/5Customer Experience Score

4/5Coverage Score

Average Monthly Cost

$49Claims Processing Score

4.1/5Policy Management Score

4/5Buying Process Score

4/5

ERGO NEXT

Best Arkansas Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.4/ 5

4.7/5Affordability Score

4.4/5Customer Experience Score

3.6/5Coverage Score

Average Monthly Cost

$50Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

Cheapest Workers' Comp Insurance in Arkansas

The Hartford and Nationwide both average $49 per employee monthly in Arkansas, the lowest rates in the state. The middle tier tells a different story. ERGO NEXT sits just $1 above the leaders at $50, making the top three essentially a cluster. Then the table jumps: Coverdash at $61 represents a 22% step up from ERGO NEXT. If rate is your only filter, the decision lives in that top cluster.

Chubb at $91 monthly is the most expensive option, 86% above The Hartford's rate. That gap warrants scrutiny before dismissing it. Chubb's higher rate reflects broader coverage triggers and underwriting for higher-risk classifications, worth comparing if your business carries high claim exposure.

Cheapest Workers' Comp Insurance in Arkansas

| The Hartford | $49 | $588 |

| Nationwide | $49 | $588 |

| ERGO NEXT | $50 | $600 |

| Coverdash | $61 | $732 |

| Thimble | $62 | $744 |

| biBERK | $65 | $780 |

| Progressive Commercial | $70 | $840 |

| Simply Business | $73 | $876 |

| Hiscox | $77 | $924 |

| Chubb | $91 | $1,092 |

Cheapest Workers' Comp Insurance in Arkansas by Industry

When we pulled workers' comp rates across 25 industries in Arkansas, one pattern emerged: The Hartford holds the cheapest rate in 14 of the 25 industries we analyzed, but its advantage is concentrated in white-collar and light-service work. ERGO NEXT wins every high-risk category, from construction ($117 per month) to agriculture ($80 per month) to transportation ($149 per month). If your employees work with their hands or operate vehicles, put ERGO NEXT at the top of your comparison list.

| Financial Services | The Hartford | $8 | $96 |

| Beauty, Body & Wellness Services | The Hartford | $9 | $108 |

| Marketing & Communications | ERGO NEXT | $9 | $108 |

| Consulting Services | The Hartford | $10 | $120 |

| Real Estate & Property Services | The Hartford | $10 | $120 |

| Other Professional Services | The Hartford | $13 | $156 |

| Tech/IT | The Hartford | $19 | $228 |

| Childcare Services | Coverdash | $20 | $240 |

| Hospitality, Travel & Tourism | The Hartford | $20 | $240 |

| Food & Beverage | ERGO NEXT | $21 | $252 |

| Healthcare & Medical | The Hartford | $22 | $264 |

| Retail & Product Rental | The Hartford | $24 | $288 |

| Nonprofit & Associations | The Hartford | $28 | $336 |

| Pet Care Services | ERGO NEXT | $31 | $372 |

| Fitness Services | ERGO NEXT | $35 | $420 |

| Education | ERGO NEXT | $36 | $432 |

| Repair & Maintenance | ERGO NEXT | $36 | $432 |

| Arts, Media & Entertainment | ERGO NEXT | $48 | $576 |

| Recreation & Sports | ERGO NEXT | $55 | $660 |

| Cleaning Services | The Hartford | $56 | $672 |

| Manufacturing | The Hartford | $70 | $840 |

| Agriculture & Natural Resources | ERGO NEXT | $80 | $960 |

| Wholesale & Distribution | ERGO NEXT | $92 | $1,104 |

| Construction & Contracting | ERGO NEXT | $117 | $1,404 |

| Transportation & Logistics | ERGO NEXT | $149 | $1,788 |

To understand who is cheapest for your company overall across all coverage types you may need, check out the industry level guides below.

How Much Is Workers' Comp Insurance in Arkansas?

At an average of $65 monthly, we found Arkansas workers' comp rates to be among the lowest in the country. But workers' comp premiums in Arkansas also vary by a factor of nearly 20 across industries. Beauty and financial services businesses pay $14 a month, while transportation and logistics operators pay $271.

The spread matters, because it tells you what underwriters are actually pricing: physical risk and injury frequency. The cheapest rates in our analysis are for marketing, consulting, and financial services, which are industries where workers rarely leave a desk. The most expensive industries are where workers operate vehicles, heavy equipment or machinery daily.

| Beauty, Body & Wellness Services | $14 | $168 |

| Financial Services | $14 | $168 |

| Marketing & Communications | $15 | $180 |

| Consulting Services | $19 | $228 |

| Real Estate & Property Services | $20 | $240 |

| Other Professional Services | $22 | $264 |

| Childcare Services | $33 | $396 |

| Food & Beverage | $37 | $444 |

| Hospitality, Travel & Tourism | $38 | $456 |

| Tech/IT | $39 | $468 |

| Healthcare & Medical | $46 | $552 |

| Retail & Product Rental | $49 | $588 |

| Nonprofit & Associations | $52 | $624 |

| Pet Care Services | $56 | $672 |

| Fitness Services | $59 | $708 |

| Education | $60 | $720 |

| Repair & Maintenance | $66 | $792 |

| Arts, Media & Entertainment | $83 | $996 |

| Recreation & Sports | $102 | $1,224 |

| Cleaning Services | $107 | $1,284 |

| Manufacturing | $127 | $1,524 |

| Agriculture & Natural Resources | $147 | $1,764 |

| Wholesale & Distribution | $163 | $1,956 |

| Construction & Contracting | $250 | $3,000 |

| Transportation & Logistics | $271 | $3,252 |

Workers' comp costs are only one part of the picture for commercial insurance you need. To get more detail into rates for all policies you may need, use the resources below.

Arkansas Workers' Comp Insurance Cost Factors

The Arkansas Workers' Compensation Commission oversees the state's workers' comp system. Arkansas uses NCCI class codes and loss costs filed by private carriers. The state's large agricultural, poultry processing and transportation industries push average rates above professional service benchmarks.

How Much Workers' Comp Insurance Do I Need in Arkansas?

Arkansas requires workers' comp for employers with three or more employees. The three-employee threshold is lower than many states, which means most Arkansas small businesses that have grown beyond a two-person operation are required to carry coverage. Review current workers' comp requirements to confirm your obligations. The Arkansas Workers' Compensation Commission enforces compliance and can impose stop-work orders.

Arkansas Workers' Comp Insurance Exemptions

Employers with fewer than 3 employees

Employers with fewer than 3 employeesBusinesses with one or two employees are exempt under Arkansas law, though voluntary coverage is available and advisable.

- Agricultural employers (limited)

Certain farm employers fall under a modified threshold; verify current rules with the Arkansas Workers' Compensation Commission.

- Sole proprietors and partners

Not required to cover themselves; may elect coverage voluntarily.

- Corporate officers

May elect to exclude themselves from coverage by written election filed with the Arkansas Workers' Compensation Commission.

- Domestic workers

Household employees are exempt from mandatory coverage requirements under Arkansas law.

- Independent contractors

Workers who qualify as independent contractors under Arkansas law are not covered as employees.

- Certain real estate agents

Agents who meet the independent contractor definition under Arkansas law may be exempt from mandatory coverage.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Federal employees in Arkansas fall under the Federal Employees' Compensation Act (FECA). Railroad workers are covered by FELA rather than Arkansas state law. Workers at commercial river port facilities in Arkansas performing qualifying maritime work may fall under the Longshore and Harbor Workers' Compensation Act. Employers with workers in these federal categories must maintain compliance with federal programs separately from any state workers' comp coverage.

While workers' comp is one of the most commonly required coverages, this doesn't mean it is the only one you need. To get a more overall picture of your coverage needs, use the guides below.

How to Get the Best Workers' Comp Insurance in Arkansas

Follow these seven steps to secure the right workers' comp coverage for your Arkansas business.

- 1

Confirm Whether Coverage Is Required

Arkansas requires workers' comp for employers with three or more employees. Count all part-time and full-time workers. If you are approaching or at the threshold, secure coverage before adding the third employee. The Arkansas Workers' Compensation Commission administers enforcement.

- 2

Identify NCCI Class Codes for Your Workforce

Arkansas uses NCCI class codes to set the base rate per $100 of payroll. Poultry processing, trucking, construction, and agricultural operations each carry distinct codes with substantially different rates. Review classifications before soliciting quotes.

- 3

Pull Three Years of Loss Runs

Carriers underwrite based on payroll and claims history. Arkansas businesses with clean records will receive more favorable quotes. Pull your OSHA 300 logs and prior policy loss runs before approaching insurers.

- 4

Request Quotes from Multiple Carriers

The Hartford and ERGO NEXT both rank at or near the top on rate and service in Arkansas. Include Nationwide for a third data point. For businesses with broader coverage needs, Coverdash is worth comparing.

- 5

Evaluate Per-Industry Rate Differences

The Hartford posts the lowest rates for financial services, health care, and professional services. ERGO NEXT leads on cost for food, beverage, pet care, and agricultural industries. Match your primary industry classification against the cheapest-by-industry data before choosing.

- 6

Bind Coverage and Notify the Commission

The Arkansas Workers' Compensation Commission requires proof of coverage before employees start work. File a certificate of insurance and keep it current throughout the policy term.

- 7

Prepare for the Annual Payroll Audit

Arkansas workers' comp policies are audited at renewal. Seasonal payroll in agriculture and food processing creates audit variability. Keep payroll records organized by class code throughout the year to minimize adjustment disputes.

Bottom Line and Next Steps

The Hartford leads Arkansas on both rate and composite score. ERGO NEXT is the runner-up, with the state's top customer experience scores and only a $1 a month rate difference from The Hartford. Health care and financial services employers will find The Hartford's industry-specific rates most competitive. Food, beverage and agricultural businesses should compare ERGO NEXT first; it holds the lowest rates in those categories

Next Steps

Arkansas's three-employee threshold means most small businesses that have grown beyond a two-person operation are required to carry coverage. If you need more help finding the right provider for you, here's how to best continue your research:

WANT TO LEARN MORE ABOUT OTHER BUSINESS INSURANCE TYPES?

Workers' comp is only one part of commercial insurance that you likely need. Check our other resources for coverage in the state below to ensure you have comprehensive coverage:

Arkansas Workers' Compensation Insurance FAQs

The Arkansas Workers' Compensation Commission can issue stop-work orders against non-compliant employers, halting all business operations until coverage is secured. Without coverage, employers bear personal liability for all employee injury costs, including medical expenses and wage replacement benefits.

Arkansas workers' comp covers employees based on where the work is performed. Remote employees who work primarily in Arkansas are covered under an Arkansas policy. Employers with remote workers in other states should confirm their policy includes those states in the covered territory, as requirements vary by state.

Arkansas uses the NCCI experience modification rate (EMR) system. An EMR below 1.0 reduces your premium; an EMR above 1.0 increases it. Employers with three or more years of payroll history and premiums above the NCCI eligibility threshold become subject to EMR calculation. Verify the current NCCI eligibility threshold with NCCI or your carrier directly, as the figure updates periodically. A clean claims record is the most direct path to a lower EMR over time.

Corporate officers in Arkansas can exclude themselves from workers' comp coverage by filing a written election with the Arkansas Workers' Compensation Commission. Sole proprietors and partners don't need to cover themselves but can elect voluntary coverage. Any opt-out election must be documented and kept on file with both the insurer and the Commission.

Workers' comp covers statutory benefits owed to injured employees under Arkansas law. Employer's liability, typically included as Part Two of a standard workers' comp policy, covers the employer against lawsuits from employees who allege negligence beyond the statutory workers' comp benefit. Both coverages are included in a standard Arkansas workers' comp policy.

Workers' comp claims generally remain in an employer's loss history for three to five years, depending on the insurer's underwriting criteria and the NCCI experience rating period. Claims used in EMR calculations typically cover a three-year window, excluding the most recent policy year. Closed claims with no ongoing payments have less impact than open or high-severity claims.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Arkansas using small business profiles with one to four employees spanning 25 industry categories and 408 subindustries. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate a MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a one to four employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work have been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes content for real pet owners.

Questions about MoneyGeek's business or pet insurance content? Reach him at connor@moneygeek.com or on LinkedIn.

Sources

- Arkansas Department of Labor and Licensing. "Basic Facts." Accessed August 5, 2026.

- Arkansas Insurance Department. "Arkansas Businesses to See Reduced Workers' Compensation Insurance Rates in 2022." Accessed August 5, 2026.

- Arkansas Senate. "Legislative Action Holds Down Workers' Comp Rates." Accessed August 5, 2026.

- Claims Journal. "Study Shows North Dakota, Arkansas, West Virginia Had Lowest Workers' Comp Rates." Accessed August 5, 2026.