MoneyGeek scores commercial property insurance providers on affordability (50%), customer experience (30%) and coverage options (20%). Each category reflects what businesses actually encounter across the full policy lifecycle, from buying to filing a claim. Price is where most businesses start the search, but it's rarely where the decision should end. The full methodology details how each category was measured and weighted.

Best Commercial Property Insurance

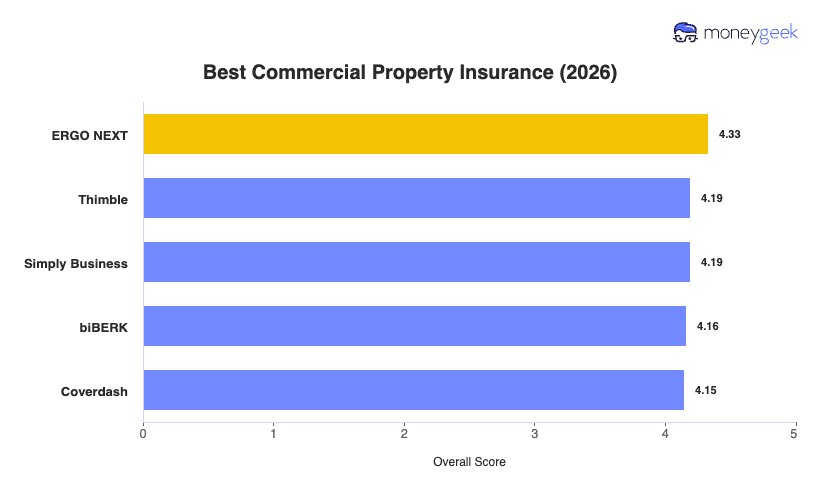

ERGO NEXT, Thimble and Simply Business rank as the best commercial property insurance providers for most businesses, based on MoneyGeek's analysis of affordability, customer experience and coverage depth.

ERGO NEXT leads overall for most businesses, but the right provider for you depends on your business type, industry and employee count.

Get matched to your best commercial property insurer and get quotes in minutes using our tool below.

Select state

Updated: May 18, 2026

Advertising & Editorial Disclosure

How We Built These Best Small Business Insurer Rankings

Top Picks: Best Commercial Property Insurance Companies

No single commercial property insurance provider is the right fit for every business. ERGO NEXT leads overall, but the right carrier depends on what the business owns or occupies, what a covered loss would actually cost the operation and how much support it needs when something goes wrong. Those factors play out differently for every operation, which is why the right answer for a solo consultant renting a single office looks nothing like the right answer for a food and beverage operator with owned equipment and inventory.

Each provider below earned its spot for a specific reason, and that reason matters more than the overall ranking when a business has a particular risk profile or set of priorities:

- ERGO NEXT: Best Overall

- Thimble: Best for Affordability

- Simply Business: Best for Customer Experience

The table below shows how they ranked overall in this analysis for a side-by-side view to ground the comparison.

| ERGO NEXT | 4.33 | 3 | 2 | 6 |

| Thimble | 4.19 | 1 | 5 | 9 |

| Simply Business | 4.19 | 7 | 1 | 7 |

| biBERK | 4.16 | 5 | 4 | 5 |

| Coverdash | 4.15 | 2 | 8 | 8 |

| The Hartford | 4.07 | 4 | 7 | 3 |

| Nationwide | 4.06 | 6 | 6 | 2 |

| Progressive Commercial | 3.90 | 8 | 10 | 10 |

| Hiscox | 3.87 | 9 | 9 | 4 |

| Chubb | 3.82 | 10 | 3 | 1 |

The summaries below lay out exactly who each provider fits best and who should look elsewhere, because overall rankings mean nothing if a provider doesn't match the specific business type, industry or operational need.

ERGO NEXT

Best Overall

ERGO NEXT prices commercial property coverage below the study average in 11 of 25 industries, making it the most consistent affordability option across the widest range of business types. It operates as a direct insurer, meaning policies are underwritten in-house rather than passed to a third-party carrier. Commercial property is available as a standalone product or bundled inside a business owner's policy (BOP) with general liability at a discount of up to 10%. Buying takes about 10 minutes online, coverage binds immediately and a certificate of insurance is available the moment you pay. BBB complaints describe claims going weeks without updates and customers having to chase adjusters for basic status information, and claims communication is its most documented weakness.

Learn More: ERGO NEXT Business Insurance Review

Thimble

Best for Low-Risk Business Areas

Thimble has the lowest rates in this analysis, coming in 11% below the study average across every business size tier. The most important thing to know before buying is that Thimble's commercial property coverage caps at $250,000 for buildings and $250,000 for contents, and building coverage is only available inside a BOP bundled with general liability. You cannot buy standalone commercial property through Thimble. Buying takes under 60 seconds online and a certificate of insurance is ready immediately after purchase. Beyond coverage caps, there is no phone number to call at any stage, claims go to a third-party administrator and customers report waiting days for email responses when something goes wrong.

Learn More: Thimble Business Insurance Review

Simply Business

Best for Customer Experience

Simply Business ranks first on customer experience in this analysis, and it works differently from every other provider here. It's a broker, not an insurer. Rather than selling its own policy, it shops your information across carrier partners including Hiscox, Travelers, Markel and Liberty Mutual, then returns competing quotes side by side in about 10 minutes. That comparison model gives businesses access to more carrier options in a single session than going directly to any one insurer, and it's the only provider in this study that routes applicants with prior claims to carriers willing to write them rather than declining outright. The tradeoff is that Simply Business has no role after you buy. Claims go directly to whichever carrier issued the policy, policy changes require contacting the carrier directly and some customers report that phone support is easy to reach during the buying process but becomes difficult to access post-purchase.

Learn More: Simply Business Insurance Review

Best Commercial Property Insurance by Industry

ERGO NEXT ranks first overall in 11 of 25 general industry categories in this analysis, with its strongest results in service-based and trade operations including construction and contracting, food and beverage, cleaning services, fitness, pet care and repair and maintenance. Simply Business leads one industry (childcare services) but ranks first on customer experience across every industry category in the study, which is the clearest differentiator for businesses where service quality and carrier access matter more than headline price.

| Agriculture & Natural Resources | Nationwide | 1 | 6 | 2 |

| Arts, Media and Entertainment | ERGO NEXT | 1 | 2 | 6 |

| Beauty, Body & Wellness Services | ERGO NEXT | 1 | 2 | 6 |

| Childcare Services | Simply Business | 1 | 1 | 7 |

| Cleaning Services | ERGO NEXT | 1 | 2 | 6 |

| Construction & Contracting | ERGO NEXT | 1 | 2 | 6 |

| Consulting Services | The Hartford | 1 | 7 | 3 |

| Education | Nationwide | 1 | 6 | 2 |

| Financial Services | The Hartford | 1 | 7 | 3 |

| Fitness Services | ERGO NEXT | 1 | 2 | 6 |

| Food & Beverage | ERGO NEXT | 1 | 2 | 6 |

| Healthcare & Medical | The Hartford | 1 | 7 | 3 |

| Hospitality, Travel & Tourism | Nationwide | 1 | 6 | 2 |

| Manufacturing | Chubb | 1 | 3 | 1 |

| Marketing & Communications | ERGO NEXT | 1 | 2 | 6 |

| Nonprofit & Associations | Nationwide | 1 | 6 | 2 |

| Other Professional Services | ERGO NEXT | 2 | 2 | 6 |

| Pet Care Services | ERGO NEXT | 1 | 2 | 6 |

| Real Estate & Property Services | Chubb | 2 | 3 | 1 |

| Recreation and Sports | ERGO NEXT | 1 | 2 | 6 |

| Repair and Maintenance | ERGO NEXT | 1 | 2 | 6 |

| Retail and Product Rental | The Hartford | 1 | 7 | 3 |

| Tech/IT | The Hartford | 1 | 7 | 3 |

| Transportation & Logistics | Chubb | 3 | 3 | 1 |

| Wholesale & Distribution | Chubb | 3 | 3 | 1 |

Dedicated resources are available to help businesses find the best commercial property insurance for their specific industry.

What Determines the Best Commercial Property Insurance for You

The best commercial property insurance isn't defined by price alone. Affordability, coverage depth and customer experience all factor into whether a policy actually works for a business when something goes wrong.

Affordability Across Your Industry and Business Size

Affordability Across Your Industry and Business SizeCommercial property insurance pricing varies more by industry and business size than most businesses expect, and MoneyGeek's analysis of over 1 million business profiles confirms it. A cleaning business with three employees pays very differently than a wholesale operation with 40, even with the same provider. The provider that prices most competitively on average won't always be the lowest-cost option for your specific industry and headcount. Providers that price competitively across a wide range of operations and business sizes tend to offer more predictability as a business grows or its property profile changes, which is why comparing rates for your actual situation matters more than relying on published averages.

Coverage That Matches Your Property's Risks

Coverage That Matches Your Property's RisksCommercial property coverage goes well beyond the building itself. A policy's real value shows up in the details, including how it values property at claim time, what causes of loss it covers and what it excludes. These are the coverage terms worth checking before buying:

- Building coverage and valuation method: Whether the policy pays replacement cost value (RCV) or actual cash value (ACV) is one of the most consequential decisions in a commercial property policy. RCV pays to rebuild or replace at today's prices; ACV factors in depreciation and often pays out considerably less than the business expects.

- Business personal property (BPP): Covers furniture, equipment, inventory and other contents at your business location. If the operation has high-value equipment, check whether per-item sublimits apply before assuming the full value is covered.

- Business income and extra expense: Covers lost revenue and additional operating costs while the business is closed for repairs. Most standard policies include a waiting period before coverage begins, commonly 72 hours, though this varies by carrier and policy. Check the restoration period limit as well, since some policies cap it at 12 months, which may not be enough for a major loss.

- Causes of loss form: A special form covers all causes of loss except those specifically excluded. Basic and broad forms cover named perils only. Special form is the stronger option for most commercial property operations and worth confirming before buying.

- Flood and earthquake exclusions: Standard commercial property policies exclude both perils. Businesses in flood- or earthquake-prone areas need separate coverage or endorsements, as these gaps don't show up until a claim is filed.

- Equipment breakdown coverage: Covers mechanical or electrical failure, which standard property policies don't include. Any operation that depends on machinery, refrigeration, HVAC or commercial kitchen equipment should confirm whether this coverage is available and at what limit.

- Ordinance or law coverage: Pays the added cost to bring a repaired building up to current building code after a covered loss. Older buildings are most exposed here, and this coverage is often sublimited or excluded from standard policies without a specific endorsement.

- Coinsurance and agreed value: A coinsurance clause requires the business to insure property to a minimum percentage of its full value, typically 80% or 90%, and penalizes underinsurance at claim time by reducing the payout proportionally. Agreed value eliminates that requirement. Confirm which applies before buying, particularly if property values have changed since the policy was written.

Customer Experience and Claims Support

Customer Experience and Claims SupportA commercial property claim is not a simple transaction. It typically involves contractors, adjusters and extended restoration timelines, sometimes weeks or months depending on the scope of the loss. How well the insurer coordinates that process matters as much as how quickly it pays. When evaluating insurers, look at how policyholders describe the claims process, not just the buying experience. An insurer that makes purchasing easy but struggles with coordination during a claim creates real financial exposure for any business that depends on its property staying operational. For an unbiased comparison point, the NAIC complaint ratio measures how often policyholders escalate disputes relative to a carrier's market share, and a consistently high ratio is worth factoring into the decision even when overall reviews are positive.

How to Choose the Best Commercial Property Insurance

Choosing the right commercial property insurance takes more than comparing premiums. The cheapest policy on paper may leave real gaps if the coverage terms don't match what the business actually owns and how it operates. These five steps will help you find the right fit.

- 1Define Your Property and Risk Profile

Start by writing down what the business owns or leases, what it would cost to rebuild or replace everything at today's prices and what would happen to revenue if that property had to close for repairs. The most common underinsurance mistake is using purchase price or tax assessed value instead of replacement cost. Those numbers are often very different, and the difference shows up at claim time. Industry type and employee count are also the two variables that most affect which provider prices your risk most competitively, based on MoneyGeek's analysis across 25 general industry categories and five employee count tiers.

- 2Determine Your Coverage Requirements

Match coverage to your actual risks, not assumptions about what a standard policy includes. A few things to confirm before comparing providers:

- If you own your building, make sure coverage pays replacement cost value (RCV), not actual cash value (ACV). ACV factors in depreciation and often pays out much less than what rebuilding actually costs.

- If the business has significant inventory, equipment or contents, check that business personal property (BPP) limits are high enough and that high-value items are not subject to low sublimits.

- If a closure would cut off revenue, confirm business income coverage is included. Check when coverage begins and how long it lasts, because both vary by policy.

- If the business is in a flood- or earthquake-prone area, get separate coverage. Standard commercial property policies exclude both perils.

- If the building is older, confirm ordinance or law coverage is included. Rebuilding to current code after a loss costs more than most business owners expect.

- 3Research Providers by Industry and Business Size

Not all carriers price every industry the same way. Use the industry and employee count data in this analysis to identify which providers are most competitive for your situation before collecting quotes. It's also worth checking whether the carrier has real experience writing policies for your industry. Coverage terms and claims handling can differ between a carrier that specializes in your business type and one that treats it as a secondary market.

- 4Evaluate Coverage Quality and Policy Terms

A premium tells you what a policy costs. The actual policy terms tell you what you are buying. For each provider you are seriously considering, check how it values property at claim time, which causes of loss form it uses, whether a coinsurance clause applies and what endorsements are available. Also ask how the carrier handles mid-term changes. Adding a location or buying major equipment during the policy period can create a coverage gap with some carriers if not reported promptly.

- 5Get Quotes to Confirm

Get quotes after you have narrowed your options, not before. A quote should confirm that a provider's pricing holds for your specific property, location and coverage needs. If a quote comes back higher than expected, check your property valuation method and coverage selections before moving on from a provider that otherwise fits.

Best Commercial Property Insurance: Bottom Line

The right commercial property insurance comes down to three questions. What do you own or lease? What would it cost to rebuild or replace everything at today's prices? And what revenue would you lose if the business had to close for 30 days? Your answers narrow the field faster than any rate comparison, because pricing and coverage depth vary more by industry and business size than most published averages reflect.

Not every provider fits every property profile, and the lowest-premium policy isn't always the best value. A policy that pays actual cash value instead of replacement cost, or uses a basic causes of loss form that excludes risks your operation actually faces, can leave a business underinsured when a claim is filed. Think about whether you want a fully digital self-service experience or agent-supported guidance, because that shapes which providers are worth your time. From there, getting two or three quotes confirms whether the right fit on paper holds up for your property and business type.

Best Commercial Property Insurance: Next Steps

For most businesses, the right starting point is getting quotes from ERGO NEXT and Simply Business. ERGO NEXT leads on affordability across 11 industries and ranks first across all five employee count tiers, making it the strongest first stop for most small businesses with physical operations. Simply Business is the strongest starting point for businesses that want to compare quotes from multiple carriers in one session before committing to a policy. If your business has high-value property, multiple locations or complex coverage needs, add Chubb or The Hartford to your list.

Recommended: If You're Ready to Get Quotes Now

By this point you should know your property profile, your coverage requirements and which providers match your industry and business size. Request quotes from at least three providers and compare both price and policy terms before committing. If a quote comes back higher than expected, check your property valuation method and coverage selections first before moving on from a provider that otherwise fits.

If You Want to Confirm Cost Before Deciding

Commercial property insurance pricing varies more by industry and business size than most published averages reflect. Use the resources below to ground your cost expectations before reaching out to any provider.

If You're Unsure What Coverage Your Property Needs

Start by mapping your actual exposure: what you own or lease, what it would cost to rebuild or replace at today's prices, what revenue depends on that property staying open and whether you have high-value equipment or inventory. Each factor points to a specific coverage type, and missing one creates a real gap in financial protection.

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.