Consulting business insurance costs vary across practice types, and for life coaching businesses specifically, the average runs $41 monthly or $498 annually across six common coverage types. For most coaches, the more relevant starting point is professional liability and general liability combined, averaging around $59 monthly based on our data. What moves your number is how you work with clients: a virtual-only practice carries almost no physical liability exposure, while coaches who meet clients in a leased office or rented venue take on third-party injury risk that insurers price accordingly.

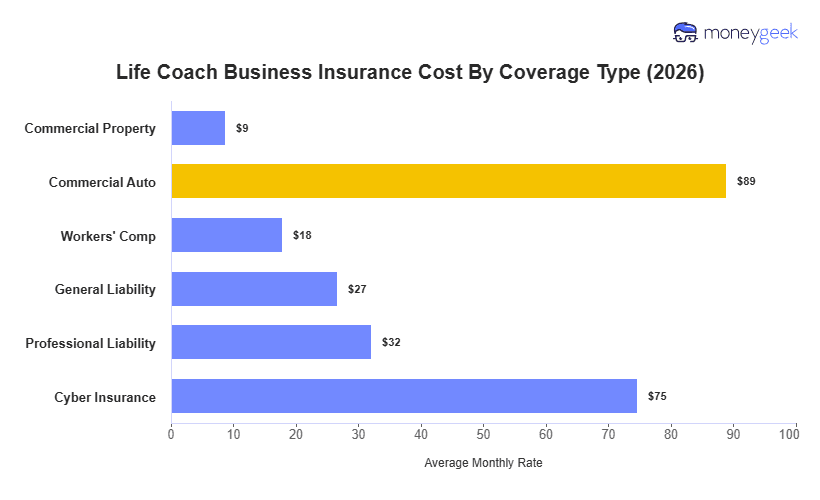

Commercial property sits at the low end at $9 per month, which fits a practice built around conversation rather than equipment or inventory. Cyber comes in at $75 monthly, the sharpest outlier in our analysis, given the sensitivity of what clients share through intake forms and session records. Commercial auto is highest at $89 monthly and matters primarily if you use your personal vehicle to travel to corporate clients or retreat venues, since personal auto policies generally don't cover business use.

The table below shows average monthly premiums for each coverage type: