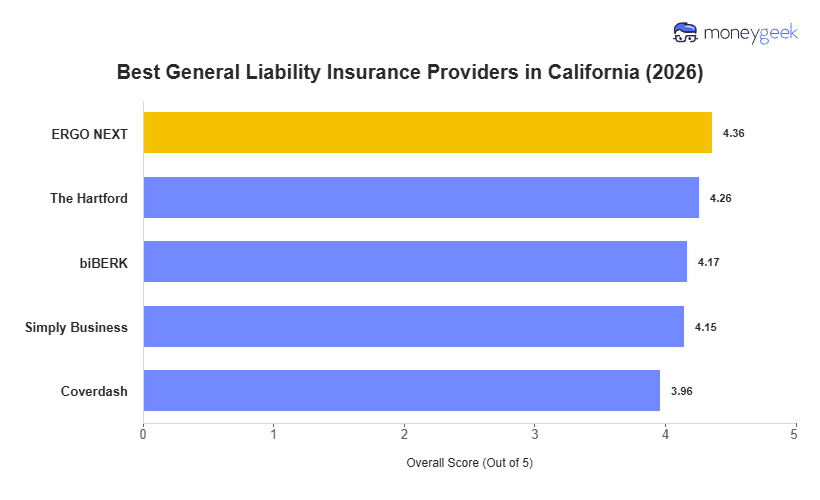

After evaluating business insurance providers based on affordability, coverage options and terms, and customer support, these five carriers deliver the most balanced California general liability insurance:

- ERGO NEXT: Best Overall, Best for Hands-on Industries

- The Hartford: Best for Office-Based Professional Services

- biBerk: Best for Recreation and Low-Risk Industries

- Simply Business: Best for Comparing Multiple Carriers

- Coverdash: Best Selection of Coverage Options

California's small businesses vary from tech consultancies in Silicon Valley to restaurants in Los Angeles, health care practices across major metros and construction firms statewide. This diversity also means that your needs and the best general liability insurance policy differ by industry, team size and location, even within the state.

We break down what sets each provider apart and who benefits most from their coverage in California: