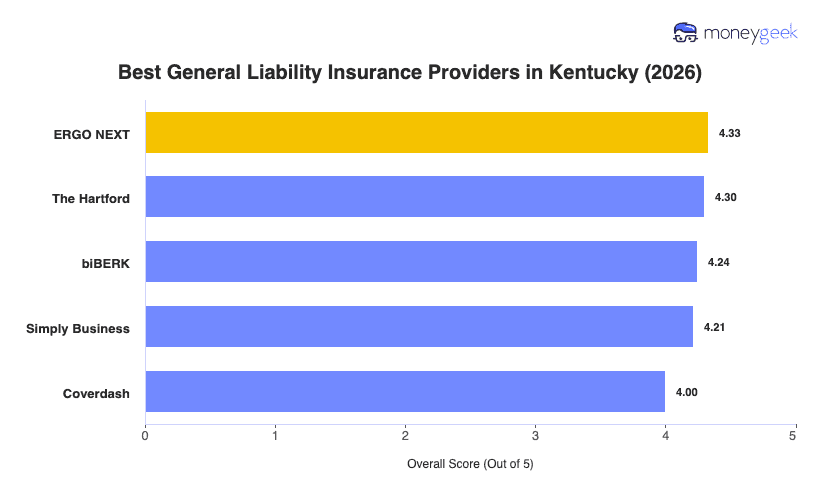

Finding the right general liability coverage in Kentucky for your business means looking beyond price. We gathered quotes with standard $1 million per occurrence/$2 million aggregate limits from 10 major insurers across 25 general industries, identifying the five providers that perform well for small businesses:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Consumer Service Businesses

- Simply Business: Best for Comparing Multiple Carriers

- Coverdash: Best for Higher-Risk or Non-Standard Businesses

The table below shows how each provider ranks on price and overall score across Kentucky. A bourbon distillery in Bardstown and an equine veterinary practice in Lexington will likely land on different providers, so use the rankings as your starting point to find the best fit for what your business actually does.