No single insurer works for every business, which is why we evaluated 10 major general liability providers across 408 business types in New Hampshire. The five companies below represent the best and most affordable options in the state, based on how well they balance price, service quality and policy flexibility.

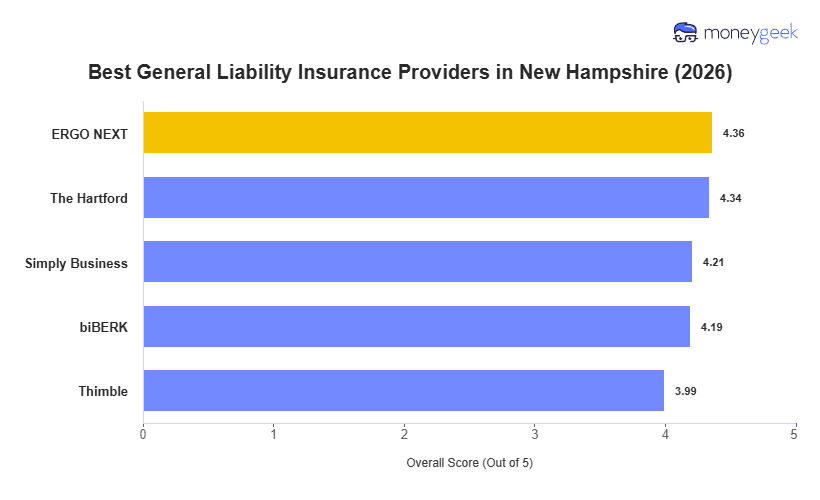

- ERGO NEXT: Best Overall, Best for Hands-On Industries

- The Hartford: Best for Professional and Office-Based Industries

- Simply Business: Best for Comparing Carriers

- biBerk: Best for Service-Based Businesses

- Thimble: Best for Freelancers and Gig Workers

The table below breaks down rates and rankings for each provider. Whether you're running a ski rental shop near Cannon Mountain or a maple syrup operation in the North Country, use it to find an insurer that fits your coverage needs and budget.