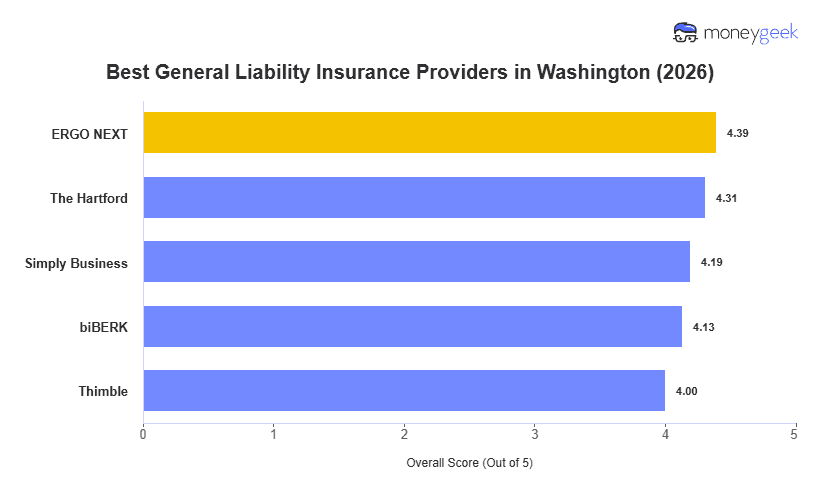

Washington small businesses don't share the same risks, budgets or coverage needs. To find the best and cheapest general liability insurers in the state, we analyzed 10 major providers across 25 general industries using the standard $1 million per occurrence/$2 million aggregate limits. These five topped our list:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best for Professional and Knowledge Businesses

- Simply Business: Best for Comparing Coverage Options

- biBerk: Best for Solo and Independent Service Operators

- Thimble: Best for Short-Term and Project-Based Coverage

The table below shows how each provider ranks and what it charges. A Spokane event photographer and a Whatcom County berry farm will likely land on different providers. What you do and where you operate in Washington affects both price and the right fit. Use the table as your starting point.