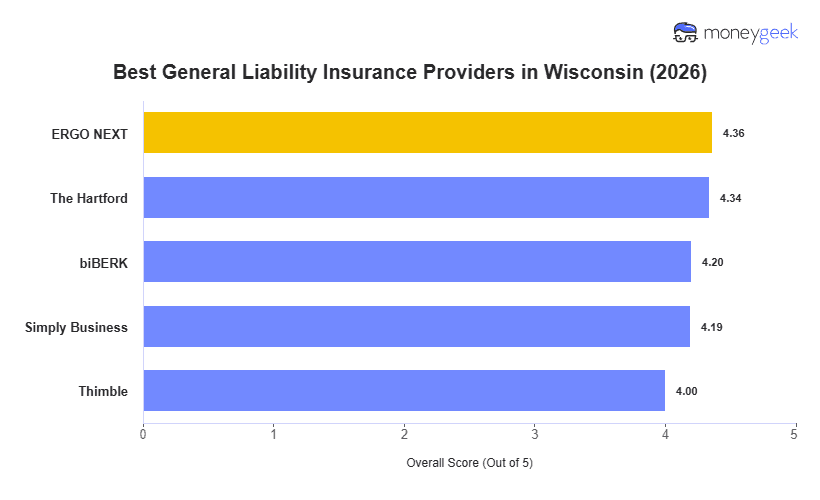

Choose the best and cheapest general liability insurance in Wisconsin by looking beyond price alone. MoneyGeek evaluated 10 insurers across 25 general industries at $1 million per occurrence/$2 million aggregate limits. No single provider fits every operation, but these five rose to the top across a range of business types and risk profiles.

- ERGO NEXT: Best Overall, Best for Service and Trade Businesses

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Consumer Service Businesses

- Simply Business: Best for Comparing Coverage Options

- Thimble: Best for Seasonal and Project-Based Businesses

Not all general liability policies are built the same, and neither are Wisconsin businesses. The table below breaks down rates and rankings for each provider. A dairy farmer adding agritourism and a Madison web developer are both looking for coverage, but where one needs broad premises protection, the other needs something leaner and more flexible.