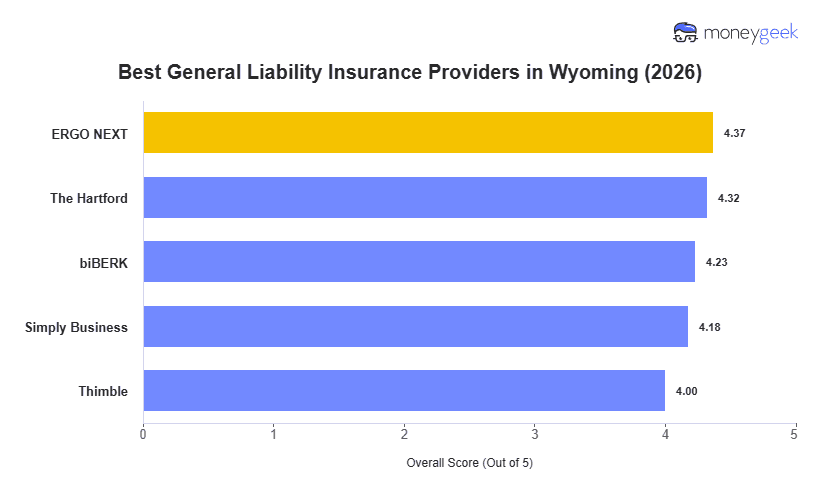

Wyoming businesses don't all carry the same risk, and no single insurer prices or covers them the same way. We analyzed 10 major general liability insurers across 408 business types at $1 million per occurrence/$2 million aggregate limits, to identify the best and cheapest options available in the state:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Service and Active-Lifestyle Businesses

- Simply Business: Best for Specialty and Hard-to-Place Coverage

- Thimble: Best for Flexible, On-Demand Coverage

Wyoming's economy is built on energy work, agriculture and tourism, and liability exposure varies widely across all three. A roughneck contractor in the Powder River Basin and a fly-fishing guide in Pinedale aren't shopping for the same coverage. The table below shows how each provider ranks on cost and coverage and helps you find the closest fit for your business.