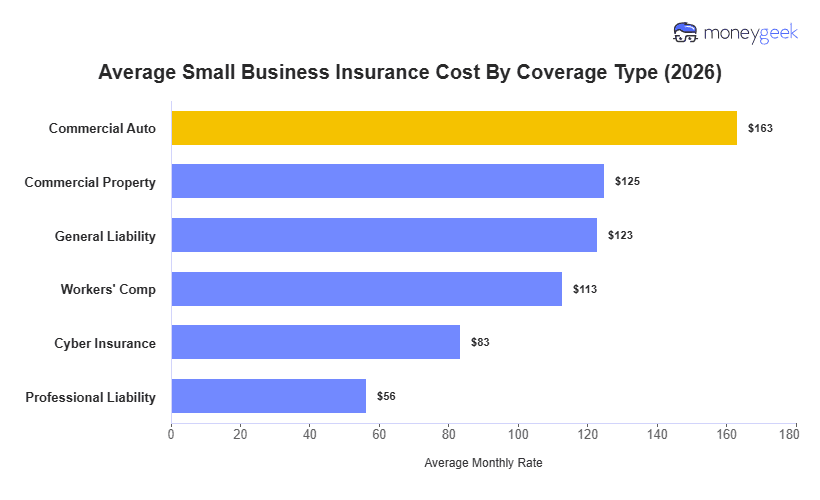

Average small business insurance costs sit at $111/mo across the six most common coverage types, but most companies pay between $60 to $110 per month for a single policy type. However, these costs represent our analysis of 1 to 4 person businesses across 408 industries, all states (including Washington D.C.), and 16 vehicle types (for commercial auto). Pricing changes widely depending on what type or types (if bundling) you buy, your industry, state, employee count and vehicles you're insuring (if this applies).

The most common bundle of a BOP policy (Business Owner's Policy) costs $221/mo with the same assumptions, combining general liability, commercial property and business interruption insurance. If you need commercial auto in addition to these coverages it is around $152/mo added on ($373/mo total) and if you're needing worker's comp, it would be $99/mo more on average to add to the bundle ($330/mo total or $454/mo if you also need commercial auto).