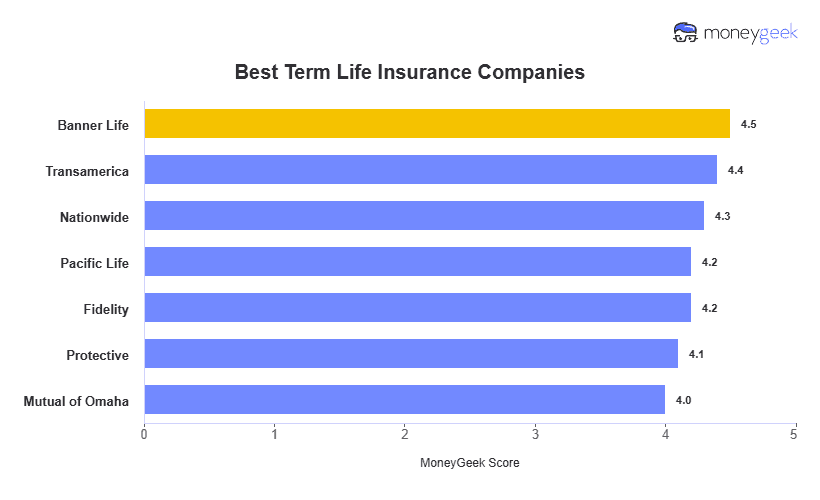

Banner Life is the best term life insurance company, with competitive monthly rates, coverage up to $10 million, term lengths up to 40 years and eligibility through age 75.

Each of the remaining companies we reviewed excels in a different area. Transamerica matches Banner Life's competitive pricing while extending eligibility through age 80. Nationwide is our top no-exam choice for buyers ages 21 to 55 who want to avoid a medical exam. Pacific Life is the best option for policy customization, offering more coverage choices and riders than most competitors at similar prices. Fidelity is our top pick for seniors because it maintains competitive rates for buyers in their 60s and early 70s. Protective is another strong choice for long-term coverage, offering policies with terms up to 40 years. Mutual of Omaha ranks highest for customer experience, supported by strong claims satisfaction, top industry ratings and service performance.